Emami Ltd is focusing more on new categories—rebranding and ramping up its presence in faster channels like e-commerce and quick commerce. But for all of this to yield meaningful results, demand needs to pick up amid a softer inflation outlook and rural rebound.

But summer, typically a good quarter for Emami, has started on a patchy note. April and May brought unseasonal rains, denting demand for core summer products such as talc powders, especially in the weather-sensitive southern and eastern states; although oils fared slightly better.

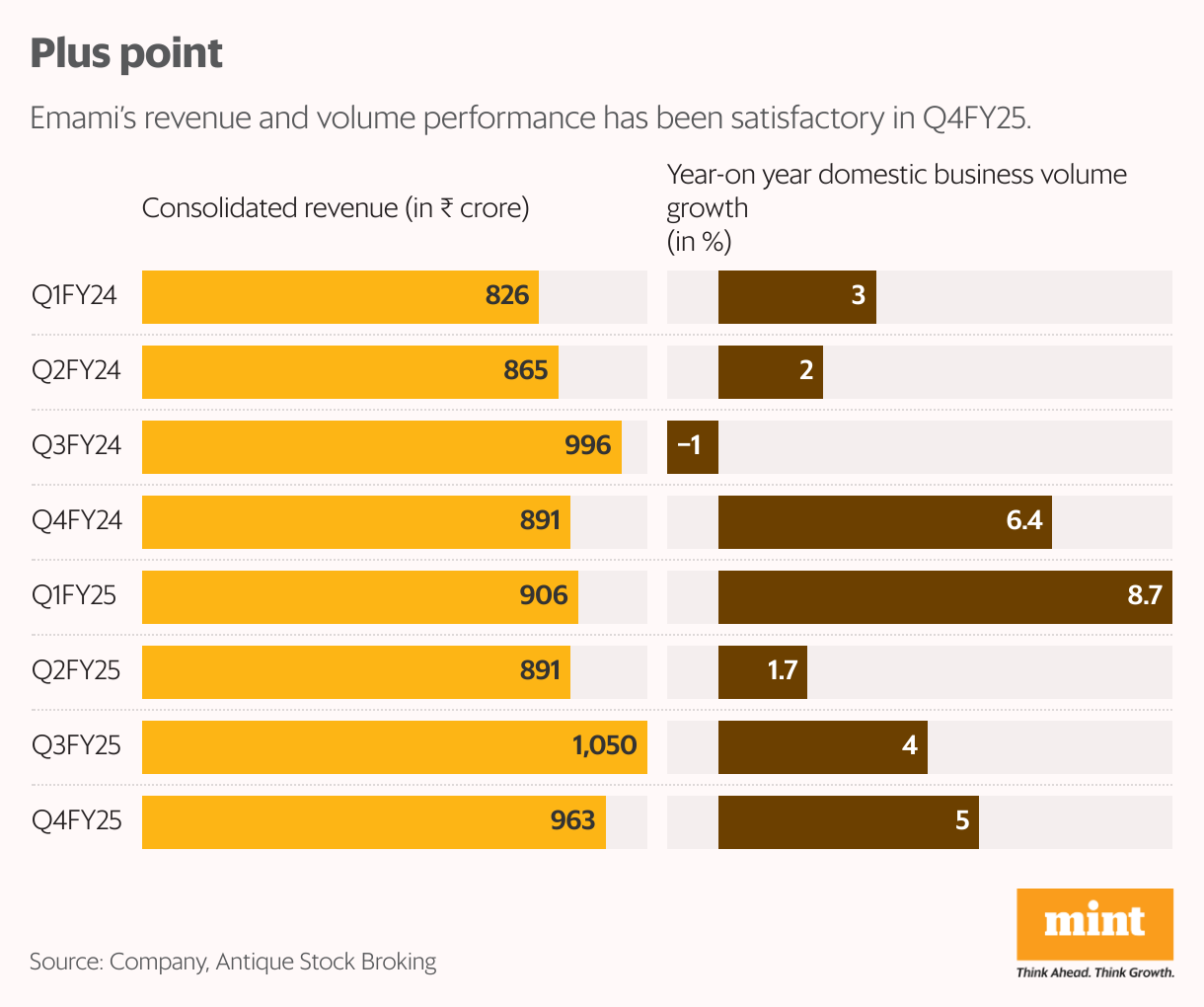

Still, the March quarter (Q4FY25) wasn’t a washout with consolidated sales up 8% year-on-year to ₹960 crore. Domestic net sales were up 9% and volume by 5%. Rural India held up, while urban demand stayed sluggish. Modern trade, e-commerce, and institutional sales, now contributing about 29% of its domestic revenue, grew steadily by 10%.

Within the core domestic portfolio, BoroPlus surged 27%, helped by an extended winter. Navratna and Dermicool together clocked a 16% rise,Zandu Care grew over 50%, now with half its revenue coming from new launches in the past two years. Even ‘Smart and Handsome’, newly rebranded, finally reversed its slide, growing 7%. International, too, bounced back, growing 6% in Q4 after a rough Q3.

Buoyed by momentum, after 25+ launches in FY25, FY26 will see more, especially in male grooming, healthcare, and skin brightening. In Q4FY25, the company entered into the skinbrightening category with the launch of Emami Pure Glow.

Pain persists

But cracks remain. Pain management was flattish in Q4FY25 and even FY25. Kesh King declined 9% in FY25, with a BCG-led strategy to be rolled out in Q2FY26. The Man Company and Brillare, Emami’s direct-to-consumer brands, clocked a revenue of ₹200 crore in FY25 but remain loss-making. The management expects strong double-digit sales growth from these businesses in FY26.

Gross margin was up slightly by 11 basis points (bps) on-year to 65.9% in Q4FY25, helped by benign commodity prices and pricing actions. Ebitda (earnings before interest, taxes, depreciation, and amortisation) grew 4%, accompanied by a 90bps drop in margin to 22.8%. One basis point is one hundredth of a percentage point.

Benign raw material prices should act as a cushion to margin, although how demand pans out is crucial.

“Valuation appears attractive at 30x 1-year forward earnings per share (EPS). However, consistency in revenue trend is a must for a sustained re-rating of the stock to the sector average,” said analysts from Jefferies India in a report on 16 May.Emami’s brand ambitions are looking brighter, but FY26 is off to a cautious start.

Leave a Comment