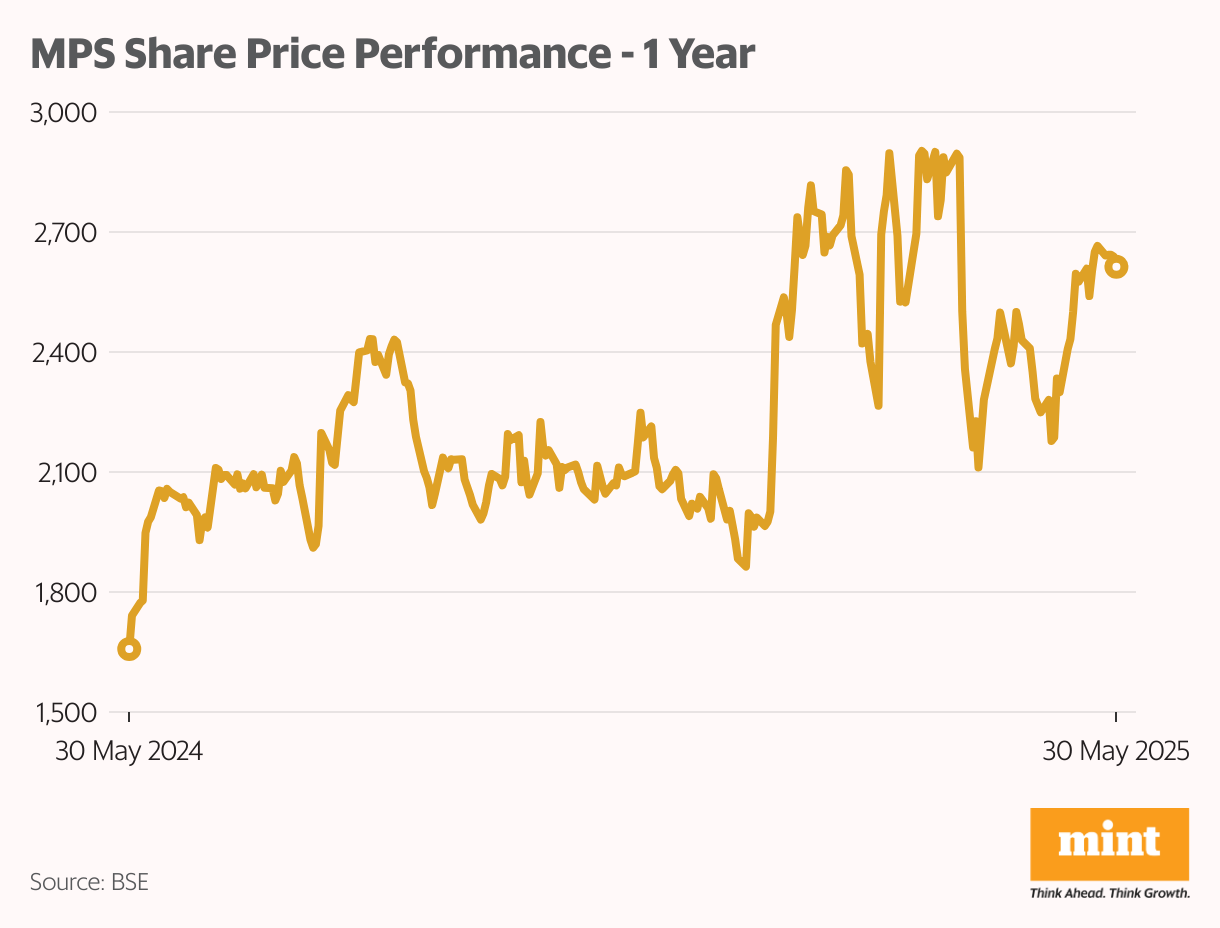

The company’s shares have surged over 50% in the past year, delivering returns that have far outpaced the BSE Smallcap Index’s 11%, on the back of a string of strong quarterly performances.

It has posted consistent growth in both revenue and net profit over the last four quarters, helped by its content solutions business.

But the story runs deeper.

The stock has delivered a staggering 1,000% return over the past five years, turning early investors into big winners.

The company’s strategic alignment with long-term trends transforming the global learning and content ecosystem has catapulted the stock into a league of its own, far beyond what earnings growth alone can explain.

So, what’s driving this rally? And more importantly, can the company sustain the momentum as it targets the next phase of growth?

In the sections that follow, we break down MPS’ growth drivers, emerging opportunities, and the challenges the company must navigate as it aims for its ambitious FY28 revenue target.

We also examine how it is leveraging artificial intelligence (AI) to sustain momentum and what that means for investors going forward.

50-year-old legacy meets innovation

For the uninitiated, MPS is a business-to-business learning and platform solutions company powering education and research for companies.

It has over five decades of experience in publishing outsourcing, three decades in eLearning, and 25 years in platform innovation. It is a combination of various leading institutions: Macmillan (1970), Tata Interactive Systems and an independent platform (Stanford, 1995).

It is also present in 15 countries, with key markets being North America, Europe, Middle East, India, and Asia Pacific.

Today, the company operates across three core segments namely content, platforms, and eLearning with content contributing over 50% to its revenue.

In the content segment, the company offers comprehensive solutions from content creation and development to editorial, design, and production. It serves some of the world’s leading publishers, learning companies, corporate clients, libraries, and aggregators via this segment.

In the platform segment, it offers configurable SaaS products that support the entire content lifecycle.

MPS has established itself as a pioneer in this space with a suite of robust platforms, including DigiCorePro, Insight, Impact Vizor, Sigma, Scolaris, THINK, and Mag+. These tools help clients manage complex content workflows efficiently and at scale.

In the eLearning segment, MPS provides cutting-edge, custom learning solutions such as web-based tutorials, simulation and game-based learning, AR/VR modules, microlearning nuggets, motion graphics, and consulting services.

From distressed buys to growth-focused deals

Inorganic growth has been a significant growth driver for MPS in the past decade. The company has made seven acquisitions over eight years, with the largest being the acquisition of AJE (American Journal Experts) in 2024.

It has also allowed it to reduce its revenue concentration to the top 10 customers from 75% in fiscal year 2014 to less than 50% by 2025. However, as most of these acquisitions were not very profitable initially, the company did not derive enough value from them until 2020.

The company has recently reconsidered its acquisition strategy. It plans to shift from acquiring distressed assets to acquiring growing entities that can contribute to the profitability quickly.

A key filter in this new approach is alignment with AI and technological innovation, ensuring that acquired companies bring in strategic AI capabilities that complement MPS’s long-term roadmap.

The company intends to maintain a standard run rate of one or two acquisitions every year in FY26 and beyond, which are not expected to require equity fundraising.

To stay prepared for any large acquisitions, the company has secured an enabling resolution for fundraising via qualified institutional placement (QIP).

This provides optionality for pursuing transformative deals in the ₹300-700 crore range and allows the company to pursue deals it might not have been able to finance solely through internal accruals and comfortable debt levels.

High growth, healthy margins underscore MPS’ strong five-year run

Over the last five years, MPS has exhibited a strong turnaround in its financial performance on the back of an increase in demand for its services.

The company’s revenue has grown at a CAGR of 17%, more than doubling from ₹332 crore in FY20 to ₹727 crore in FY25. Net profit also has grown in tandem, rising from ₹60 crore to ₹149 crore over the same period, showcasing consistent profitability.

Margins have shown a steady improvement as well. Operating profit margin of the company has grown from 24% in FY20 to 29% in FY25, reflecting better cost efficiencies and improved scale. Similarly, net profit margin has risen from 18% in FY20 to consistently stay above the 20% mark.

This improved profitability is reflected well in its return ratios.

The company’s return on equity (RoE) stands at a robust 25.9% as of FY25, indicating a sharp enhancement in shareholder value creation. Return on capital employed (RoCE), also is significantly high at 35.3%, supported by the company’s lean capital structure.

On the balance sheet front, MPS has maintained a strong foundation. The company’s borrowings have remained minimal, indicating a deliberately debt-light strategy.

At the same time, it has judiciously expanded its asset base. Fixed assets have grown from ₹115 crore in FY20 to ₹346 crore in FY25, indicating significant capital investment.

The company has also paid consistent dividends to shareholders.

MPS’ 4-year average dividend payout ratio stands at 73%, indicating that the company returned a significant portion of its profits to shareholders, while its 4-year average dividend yield stands at 3.7%.

While the yield has moderated to 2.92% in FY25, this has been largely due to rising share prices rather than lower payouts.

The stock is also on the radar of super investors.

As per the latest shareholding pattern data, investor Mukul Agrawal holds a 4.5% stake in MPS, underscoring institutional and high-net-worth interest in the company.

Tapping into a $600 billion opportunity with AI at the core

The content industry is currently experiencing powerful structural tailwinds driven by the rising adoption of AI/ML technologies and automation. With the opportunity pegged at $600 billion, the scope for growth is vast, particularly for players such as MPS.

To capitalize on this opportunity, the company is positioning itself as a frontrunner in digital learning by embedding AI at the core of its business strategy.

Areas such as real-time translation, intelligent language editing, content generation, and accessibility services are already seeing strong demand, and MPS plans to capitalize on these trends by broadening its portfolio of AI-enabled solutions.

Its research and development hub, MPS Labs, is at the forefront of this effort, leveraging AI, machine learning, natural language processing (NLP), and cloud-based technologies to develop tools that support the entire content lifecycle.

It also plans to launch a dedicated AI and data practice unit by FY26. This unit will deliver market-facing, AI-driven solutions and is expected to function as a parallel revenue engine, reinforcing MPS’s long-term growth strategy.

Management remains confident that these AI-driven initiatives will scale meaningfully in the years ahead.

MPS’ vision for FY28

While being a market leader in the $600 billion digital learning and content solutions space may seem far-fetched for MPS at this stage, the company has set its sights on a more near-term, yet ambitious goal—reaching ₹1,500 crore in revenue by FY28.

Management views this target as well within reach, given the vast opportunity the sector presents.

At the heart of this roadmap is the company’s “Going Gestalt” strategy. The strategy is an integrated, principle-driven approach designed to unlock synergy across its business segments and make MPS greater than the sum of its parts.

To achieve its targets, MPS is relying on several strategic growth levers.

The company is targeting an organic growth rate of 10–12%, supported by focused investments in new capabilities and expansion of high-potential accounts.

It also plans to focus on expanding Strategic Customer Partnerships (STAR accounts), with a goal to increase the number of STAR accounts to 100 by the end of FY25. This strategy is expected to bring significant progress in organic growth and margins.

Product innovation is another critical focus area. In 2025, MPS plans to launch enhanced versions of its SaaS offerings to further boost its recurring revenue base.

Finally, the company plans to pursue its updated acquisition strategy that extends its geographic footprint and market presence.

Priority regions include India, the Middle East, Australia, China, Brazil, and South Korea.

The acquisition of AJE is expected to play a significant role in accelerating progress toward the company’s Vision FY28.

What could derail the momentum?

While MPS has delivered strong growth over the last five years, several structural challenges remain.

The company faces client concentration risk as it derives all its revenue from the publishing industry, with a significant portion coming from its top five clients who contribute around 36% to the company’s total revenue.

This heavy dependence on a few clients increases its vulnerability to contract losses or budget cuts.

Additionally, it also faces concentration risk with respect to geographies. A large chunk of the company’s revenues comes from specific geographies (45% from North America and 28% from the UK/Europe). Any economic slowdown in these regions could materially impact performance.

There is already a slowdown underway in the US and Europe, with projections pointing to weak or very weak growth in 2025. This could weigh on the company’s financial performance.

The IT industry, too, is facing headwinds across several key areas including hiring, revenue growth, and discretionary spending which could further impact business momentum.

Conclusion

MPS has quietly transformed itself from a niche content player into a high-growth, high-margin digital solutions company.

Over the past few years, it has steadily scaled its capabilities across digital learning, AI-driven platforms, and enterprise solutions.

For investors with a long-term horizon, the stock presents a compelling bet, offering a rare combination of profitability and innovation-led growth.

However, valuations appear stretched. The stock is currently trading at a price-to-earnings (P/E) ratio of 31x, nearly double its 10-year average historical P/E of 16.4x, suggesting that much of the optimism may already be priced in.

Investors should be mindful of the risks, as any slowdown in growth or external headwinds could lead to sharp price corrections given the high valuation.

Ayesha Shetty is a research analyst registered with the Securities and Exchange Board of India and a certified Financial Risk Manager.

Disclosure: The author does not hold shares in any of the companies discussed. The views expressed are for informational purposes only and should not be considered investment advice. Readers should conduct their own research and consult a financial professional before making investment decisions.

Leave a Comment