This vulnerability resurfaced once again as the post-pandemic credit boom lost momentum in FY25. Initially driven by low interest rates, credit growth began slowing as borrowing costs rose and economic activity weakened. This shift strained borrower repayment ability, increased asset quality stress, and severely hit profitability across the sector.

To limit further damage, many lenders opted to write off bad loans and reset their books. The intent was to enter FY26 with a cleaner slate, as the industry looks ahead to a potential recovery.

Spandana Sphoorty took a similar approach. In FY25, it wrote off loans worth ₹1,618 crore—a move that dented profits. However, with most of the clean-up now behind it, it is positioning itself for a turnaround in FY26. So, where does Spandana stand after this reset?

AUM contracts

Let’s start with assets under management (AUM), which declined sharply by 43% year-on-year to ₹6,819 crore in FY25. Disbursements also fell 48% to ₹5,605 crore, as Spandana adopted a cautious lending stance. This is evident from the AUM per branch, which fell from ₹7.3 crore in March 2024 to ₹3.8 crore in March 2025.

This conservative approach directly contributed to the drop in the overall loan book. The management said FY25 was one of the most challenging periods for the microfinance industry. Multiple headwinds—including higher borrower leverage, weakening of the Joint Liability Group model, deteriorating borrower discipline, and sociopolitical interference—forced lenders to tighten credit norms and proceed with greater caution.

The impact of this is also visible in customer numbers, which fell from 3.3 million in March 2024 to about 2.5 million by March 2025. However, now the company remains confident of reviving growth in FY26.

It plans to grow its AUM book by 20%, driven by a similar increase in disbursements, most of which is expected in the second half of FY26. The company now plans to lend to quality borrowers—who currently account for 51% of its borrower base as per internet lending regulations—to support the future growth.

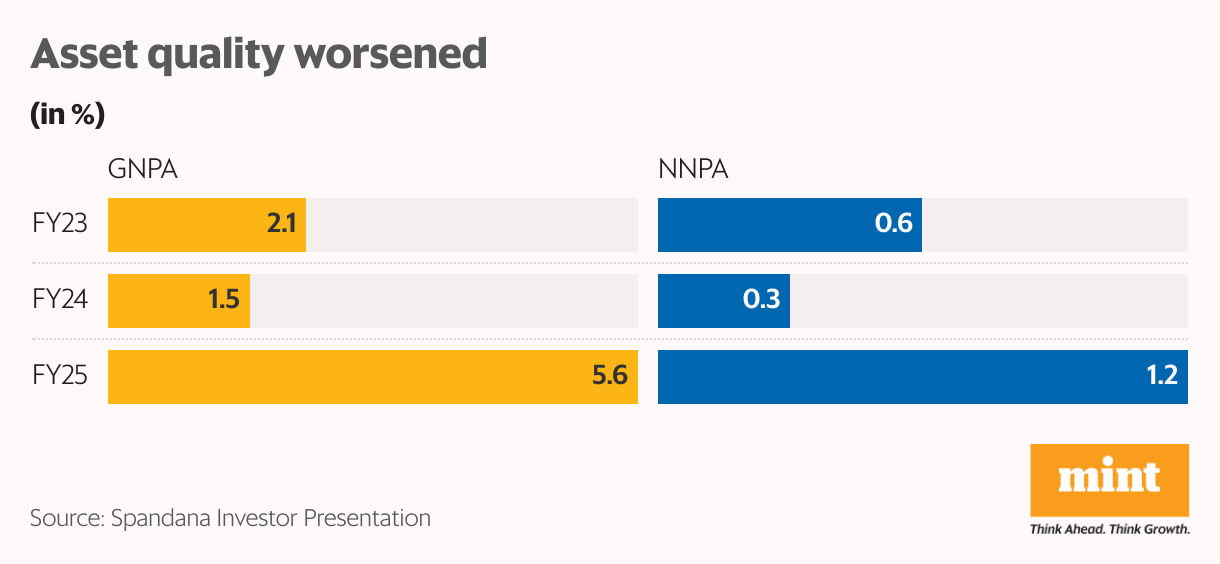

Asset quality worsens

Not just AUM, but asset quality stress also increased—a trend often seen in times of stress in the microfinance industry. Spandana impairment cost—unrecoverable loans—rose from ₹259 crore (in FY24) to ₹1986 crore in FY25.

Gross non-performing assets (GNPA) increased by 4.1 percentage points to 5.6%, while net NPAs rose by 0.9 percentage points to 1.2%. On the positive side, Spandana continues to maintain a healthy provision coverage ratio of 80%.

The management attributed much of the stress to elevated field-level attrition, which hurt operational efficiency and contributed to rising delinquencies. To strengthen collections, the company has now deployed around 700 loan officers, who will focus on recovery from 90+ day old loans and the write-off pool.

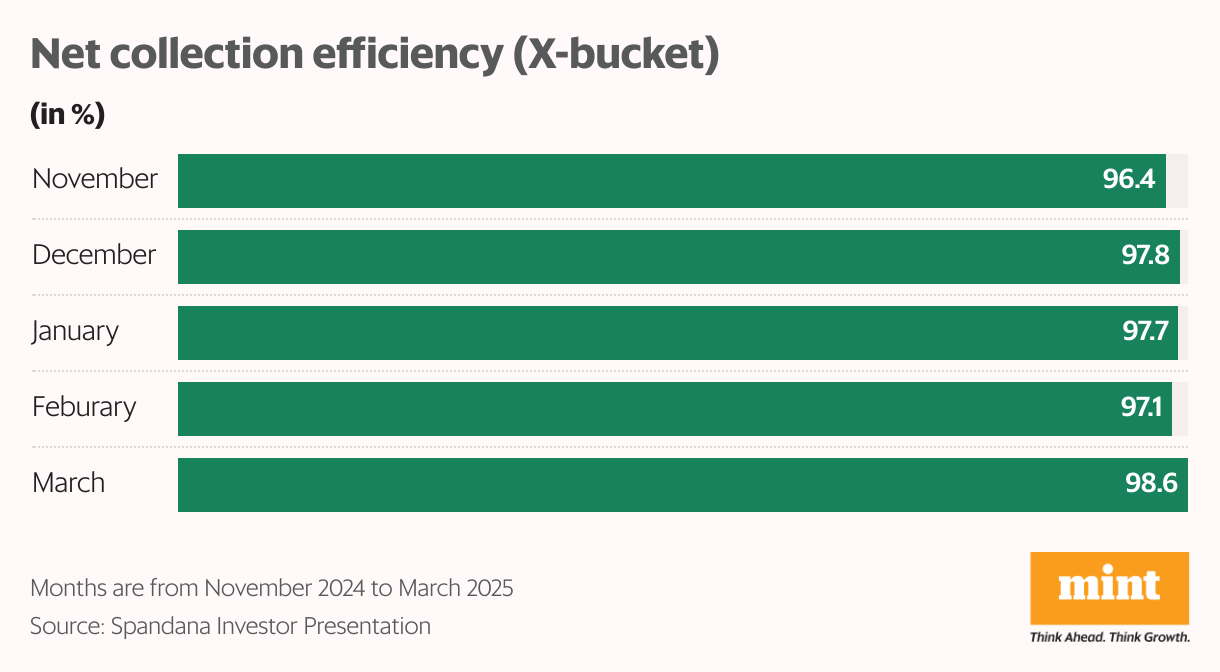

Early recovery signs

Despite a challenging year, Spandana is starting to see early signs of recovery. Gross collection efficiency declined from 94% in Q1 to 90.9% in Q4FY25. But the company highlighted an improving trend in net recovery from bad assets.

Net collection efficiency for loans overdue by more than 90 days (called X-Bucket) improved from 96.4% (Nov-24) to 98.6% in March 2025. Interestingly, branches with a weekly repayment model reported even higher collection efficiency of 99.3% in March.

As a result, Spandana now plans to scale up its weekly-model branches, which are showing better collection performance. The company believes improving collections to about 99% helps support profitability going forward.

Recovery from 90+ day past-due accounts has also picked up meaningfully, rising from ₹11 crore in Q1FY25 to ₹52 crore in Q4 FY25. In total, Spandana recovered over ₹90 crore in the last fiscal. In FY26, the company expects a further recovery, aided by a dedicated team and the early arrival of the monsoon, which typically supports rural cash flows.

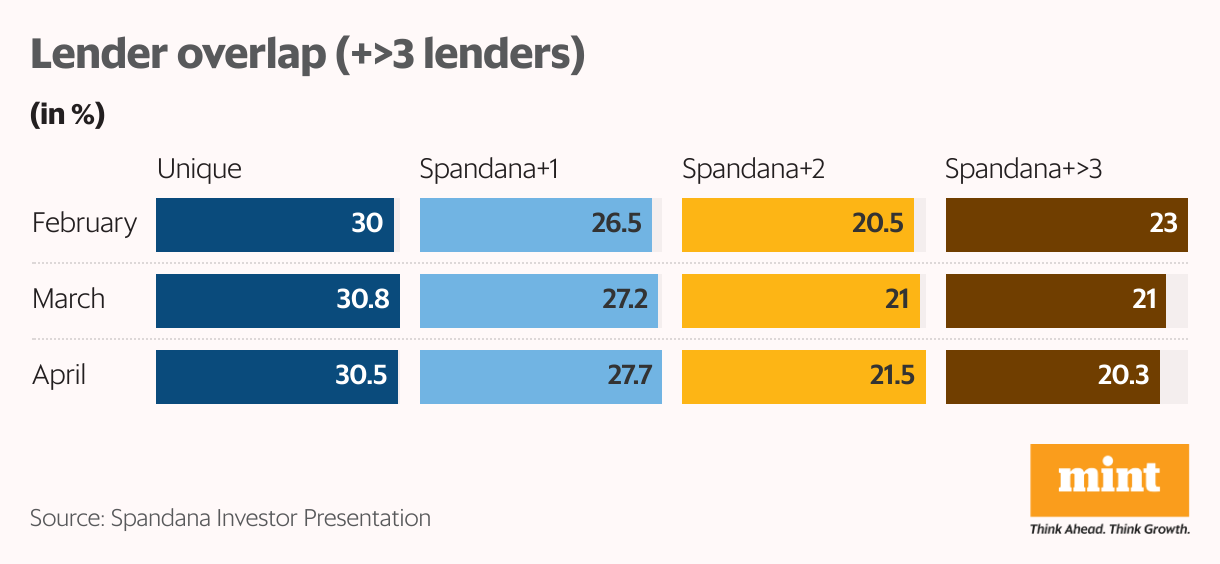

Strict credit filters to address borrower leverage

Lender overlap—the proportion of borrowers taking loans from three or more MFIs, including Spandana, has also shown signs of improvement. Lender overlap declined from 23% (Feb-25) to 20.3% in April 2025, indicating some relief on the leverage front.

To tackle the issue further, Spandana has decided on stricter credit filters. It will now cease lending to borrowers with overdue loans exceeding 60 days with any regulated entity, where the loan amount exceeds ₹3,000. Additionally, it will also avoid lending to borrowers who have availed a loan in the past 12 months, effective June 2025.

Profitability severely hit

While green shoots are visible, elevated stress levels kept credit costs high, which impacted profitability in FY25. The company’s total income declined by just 3% to ₹2,424 crore, indicating a relatively stable topline. Net interest income also fell by 5% to ₹1,228, as the net interest margin contracted by 1.3 percentage points to 12.8%.

However, the bigger concern was on the operating front. Pre-provision operating profit dropped sharply by 35% to ₹608 crore, as the cost-to-income ratio rose to 60.6% from 43.5% in FY24.

This situation was further aggravated by impairment, which rose from ₹259 crore (FY24) to ₹1,986 crore (including write-offs of ₹1,618) in FY25. As a result, the company moved from a profit of ₹501 crore in FY24 to a net loss of ₹1,035 crore in FY25. Needless to say, the return ratios—return on assets and return on equity—turned negative.

Capital position stays strong

Spandana’s net worth declined from ₹3,707 crore to ₹2,633 crore due to the heavy loss in FY25. However, its capital adequacy remains well above regulatory norms, with a capital-to-risk-weighted assets ratio (CRAR) of 37.1% as of March 2025, well above the RBI’s mandated 15%.

Liquidity healthy; rights issue planned

The company’s liquidity position continues to offer comfort. It reported a cash balance of ₹2,030 crore as of March 2025, enough to meet short- and medium-term requirements.

Additionally, shareholders approved a ₹750 crore capital raise in March 2025, and the company plans to raise further capital in Q2 FY26 via a rights issue, with promoter participation, which signals confidence in a potential turnaround.

Valuation factors in stress

Spandana’s share price has declined 64% in the last one year, currently trading at ₹262. This correction has largely priced in many of the concerns, with the stock now valued at a price-to-book (P/B) multiple of 0.7x, significantly below its 10-year median P/B of 1.5x.

Going forward, a sustained recovery in key metrics—particularly in asset quality, disbursement growth, and collection efficiency—will be crucial to re-rating, with most of this expected to unfold from the second half of FY26.

Madhvendra has over seven years of experience in equity markets and has cleared the NISM-Series-XV: Research Analyst Certification Examination. He specialises in writing detailed research articles on listed Indian companies, sectoral trends, and macroeconomic developments.

Disclosure: The writer does hold the stocks discussed in this article. The purpose of this article is only to share interesting charts, data points, and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educational purposes only.

Leave a Comment