Analysts had already flagged that the FY27 target seemed ambitious without inorganic growth. So, with the guidance now pushed to FY28, does this deferment signal deeper trouble? What does it mean for investors?

Strong foundations

Tata Communications owns the world’s largest fibre network of over 5 lakh kilometres of undersea fibre, and more than 2.1 lakh kilometres of land fibre. It holds a near-monopoly, with over 70% of global telecom companies using this network to provide mobile services. The network also supports 80% of global cloud players and 25% of the world’s internet routes.

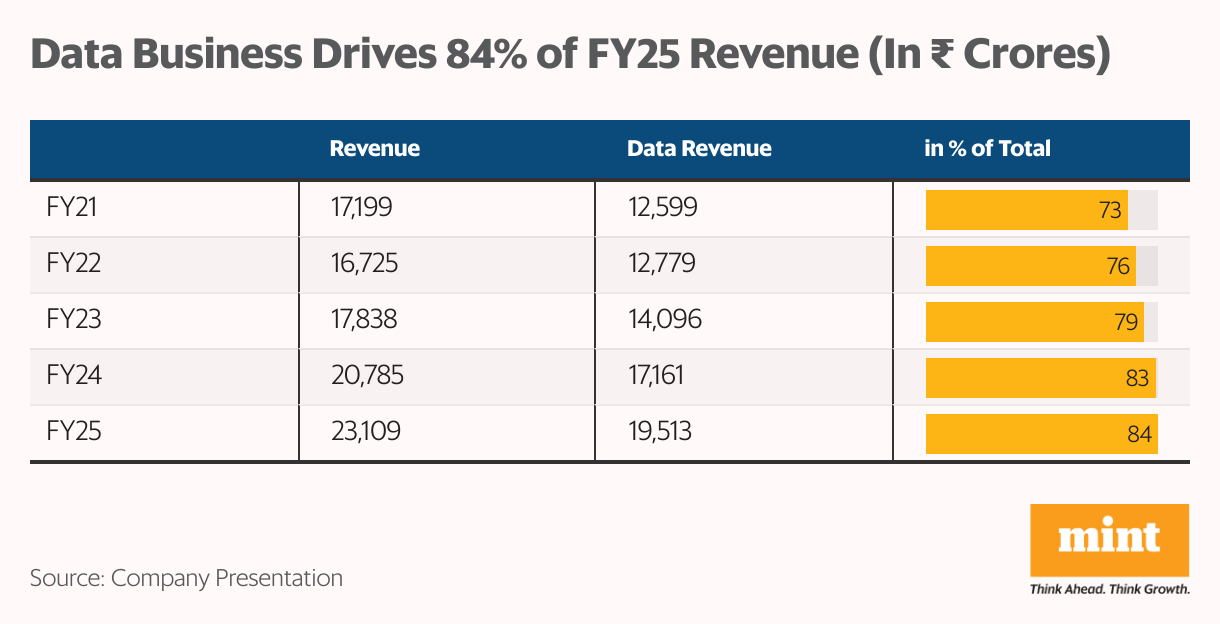

The company recorded a revenue of ₹23,109 crore in FY25 against ₹20,785 crore in FY24. Of the ₹23,109 crore, the majority 84% ( ₹19,513 crore), came from data revenue, while the remaining 16% came from voice and other sources. Data revenue is further categorized into core connectivity (data pipes) and digital platforms. Digital platforms, including cloud, cybersecurity, and IoT, are experiencing steady traction, driven by long-term demand trends.

Core connectivity, digital offerings

Digital platform revenue almost doubled to ₹9,171 crore in FY25, from ₹4,977 crore in FY24, accounting for 47% of its data revenue, up from 29% a year ago. At the same time, core connectivity revenue declined 15% to ₹10,342 crore, and now accounts for 53% (down from 71% in FY24) of data revenue. While cable cuts impacted H1 FY25, the broader trend indicates a structural slowdown in core connectivity.

Industry-wide annual price declines of 10-15%, combined with companies shifting from legacy internet calling systems to cloud-based tools (such as Zoom), and price shifts from MPLS (a private, secure, but expensive technology) to cheaper internet-based solutions, continue to weigh on its performance.

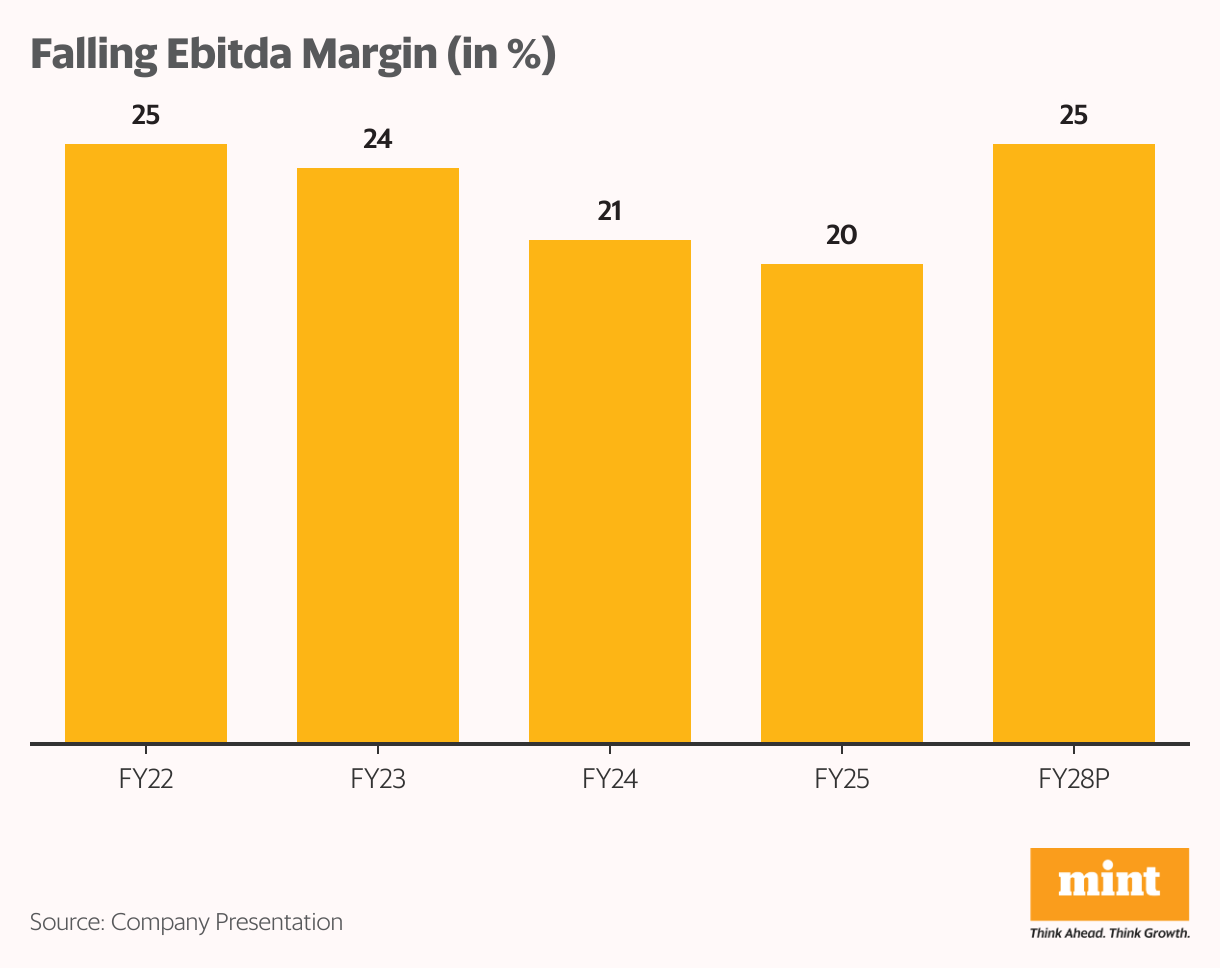

Nonetheless, core connectivity still contributes the bulk of Ebitda, accounting for ₹4,538 crores at a margin of 43.6%. However, this was offset by a ₹886 crore Ebitda loss (-9.7% margin) in the digital business, as it continues to be in investment mode. As a result, its margin fell from 25% in FY22, to 20% in FY25.

Digital ambitions

The data business has gained momentum, driven by strategic acquisitions. The earlier ₹28,000 data revenue target implied a steeper 19% compounded annual growth rate (CAGR) between FY23 and 27, which was even higher than the 11.6% CAGR recorded during FY21 to FY25.

This projection assumed enterprises’ demand for integrated network, cloud, and security solutions would accelerate. This was subject to macroeconomic and geopolitical headwinds. Given these headwinds, a delay of a few quarters may not alter the long-term outlook.

Notably, the digital segment is expected to be the main growth driver. It is projected to contribute ₹18,200 crore, accounting for 65% of the ₹28,000 crore data revenue target. This implies a 26% CAGR, slightly higher than the 25% CAGR achieved during FY21-25. Meanwhile, core connectivity revenue is expected to decline.

Also read: Tata Communications shifts focus: Can it transform into a digital powerhouse?

New growth engines

One-third of the revenue growth is expected to be driven by new services, strategic digital investments, and shifts in digital capabilities. The company has identified five additional growth segments with a market size of over $40 billion.

One such bet is the Unified Cloud Network, launched in FY23, which already has an annual recurring revenue (ARR) of over $30 million. Tata expects the total addressable market to grow to $8 billion by FY30 from the current $3.5 billion. It is targeting 30% cost efficiency, a nine-times faster connection setup, and a 20-times reduction in error rate.

Next is the customer interaction suite (CIS), which is currently growing at a 15% CAGR and has an ARR of $30 million. It estimates the addressable market will double from $10 billion to $20 billion by FY30. CIS enables outcome-based, personalized interactions within the customer experience (CX) ecosystem.

Then comes the secure access service edge (SASE), which is growing at a 15% CAGR and has an annual revenue of $50 million. The current market size is $16 billion and is expected to grow at 17% CAGR through FY30.

Additionally, the company has recently entered two new markets. AI Cloud is the fastest-growing, with an expected CAGR of 82% and a current market opportunity of $1 billion in India. Its SaaS platform—Digital Fabric—addresses a $10 billion market, projected to grow at a 15% annual rate.

Also Read: As India tightens data rules, top tech companies dish out a new offering: compliance as a service

Customer base expansion

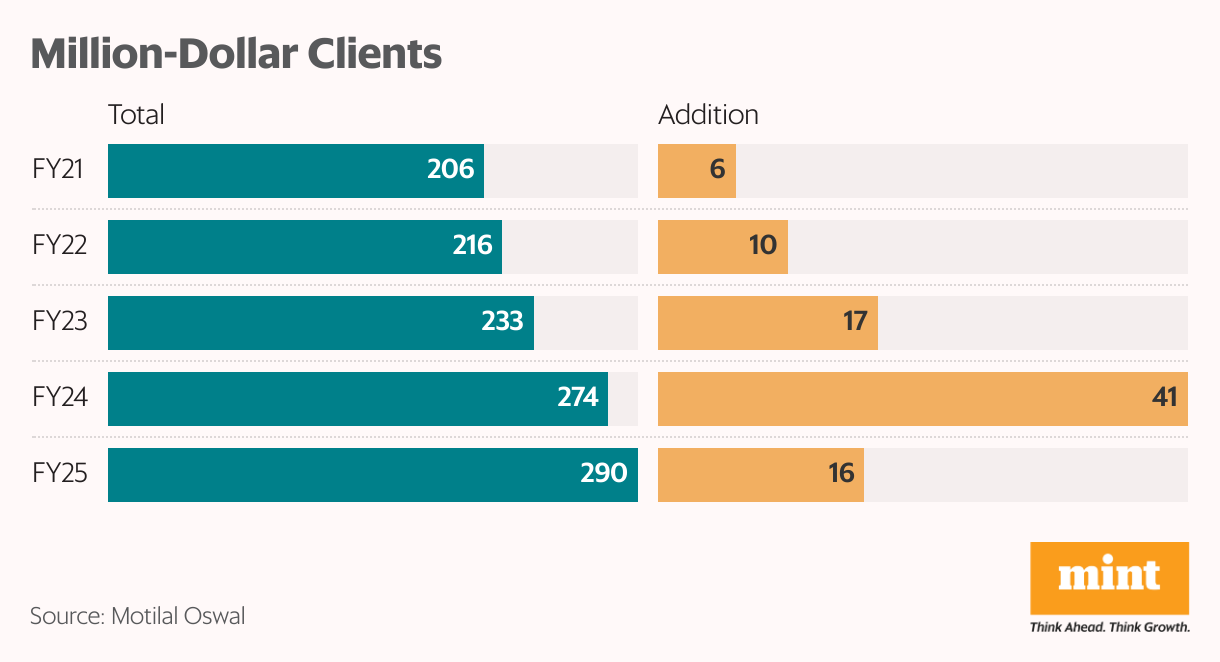

It’s not just about entering new tech areas—it is also expanding its customer base. In FY25, the company added 16 clients that can generate at least $1 million in annual revenue, which typically takes around 18 months. It now has 290 such accounts, 1.4x more than in FY21.

The company expects to add 15–20 such clients annually, each with the potential to bring $10–50 million. More than 60% of its order book consists of multi-year deals, providing revenue visibility. It expects 75-80% of the incremental revenue to come from existing clients through cross-selling.

Among larger clients, 70% of those generating over $5 million annually use more than three Tata Communications services. In addition, 53% (155 out of 290) of million-dollar accounts derive over 50% of their spend from digital services. These high-value accounts made up 57% of the FY25 order book, proving strong growth potential.

Profitability still a work in progress

As with any emerging segment, the digital business remains loss-making, with an Ebitda loss of ₹886 crore in FY25. Management’s first milestone is break-even, with margin expansion expected in FY26, aided by cost optimization and operating leverage.

Post break-even, management is targeting near-term margins of 4-6%, with a long-term goal of achieving double-digit margins and ₹1,500 crore in Ebitda. This will require adding over ₹2,300 crore in incremental Ebitda. However, Motilal Oswal believes that achieving this target will be challenging due to low margins in reselling services.

Balancing growth with asset monetization

To fund its ambitions, Tata Communications is also monetizing non-core assets. For instance, it sold its ATM subsidiary at a gain of ₹431 crore. It also has monetized real estate assets, raising over ₹1,000 crores over the last five years.

It plans to monetize two-three large additional land parcels, including those in Chattarpur and Greater Kailash. However, sale timelines can be long—the latest deal took five years to close. Proceeds from the transaction will be used to bring down leverage.

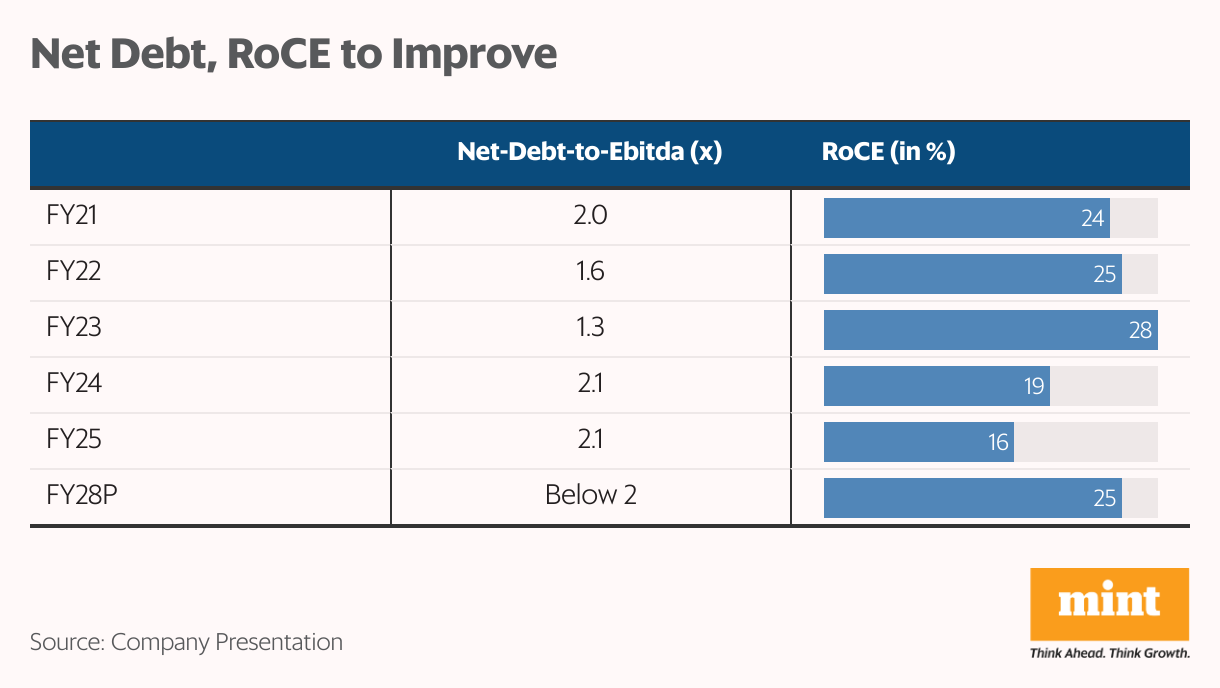

The continued expansion has also led to an increase in net-debt-to-Ebitda, from 1.3 times in FY23 to 2.1 times in FY25. Management expects this to improve to below 2x within the next two quarters.

Tata Communications is also looking to enhance capital efficiency.Its RoCE fell from 28% (FY23) to 16% in FY25, mainly due to investments in digital business. As the digital business turns profitable, management expects RoCE to rebound to 25%, and Ebitda margins to rise to 23–25%. Exiting low-margin contracts is also likely to help enhance returns and improve efficiency.

Also Read: Adani Ports bets big on doubling revenue by FY29. But execution is everything.

Valuation full, but triggers ahead

From a valuation perspective, it trades at a price-to-earnings multiple of 43, a 20% premium to its 10-year median of 35. For now, the shift in timeline appears priced in, with the stock trading largely flat. However, investors may need to tone down near-term growth expectations.

While the delay warrants caution, the long-term strategy remains intact if execution stays on course. Break-even in digital, improving margins, and a rebound in RoCE could be key triggers to watch. In contrast, risks like slower expansion, higher costs, supply chain uncertainties, and execution challenges can undermine the assumptions.

For more such analysis, read Profit Pulse.

About the author: Madhvendra has over seven years of experience in equity markets and has cleared the NISM-Series-XV: Research Analyst Certification Examination. He specialises in writing detailed research articles on listed Indian companies, sectoral trends, and macroeconomic developments.

Disclosure: The writer does not hold the stocks discussed in this article. The purpose of this article is only to share interesting charts, data points, and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educational purposes only.

Leave a Comment