Tata Motors Ltd has started FY26 on a bumpy road, with its key subsidiary Jaguar Land Rover (JLR) navigating multiple headwinds — from US tariffs and tough market conditions in China to ongoing uncertainty around the electric vehicle (EV) transition.

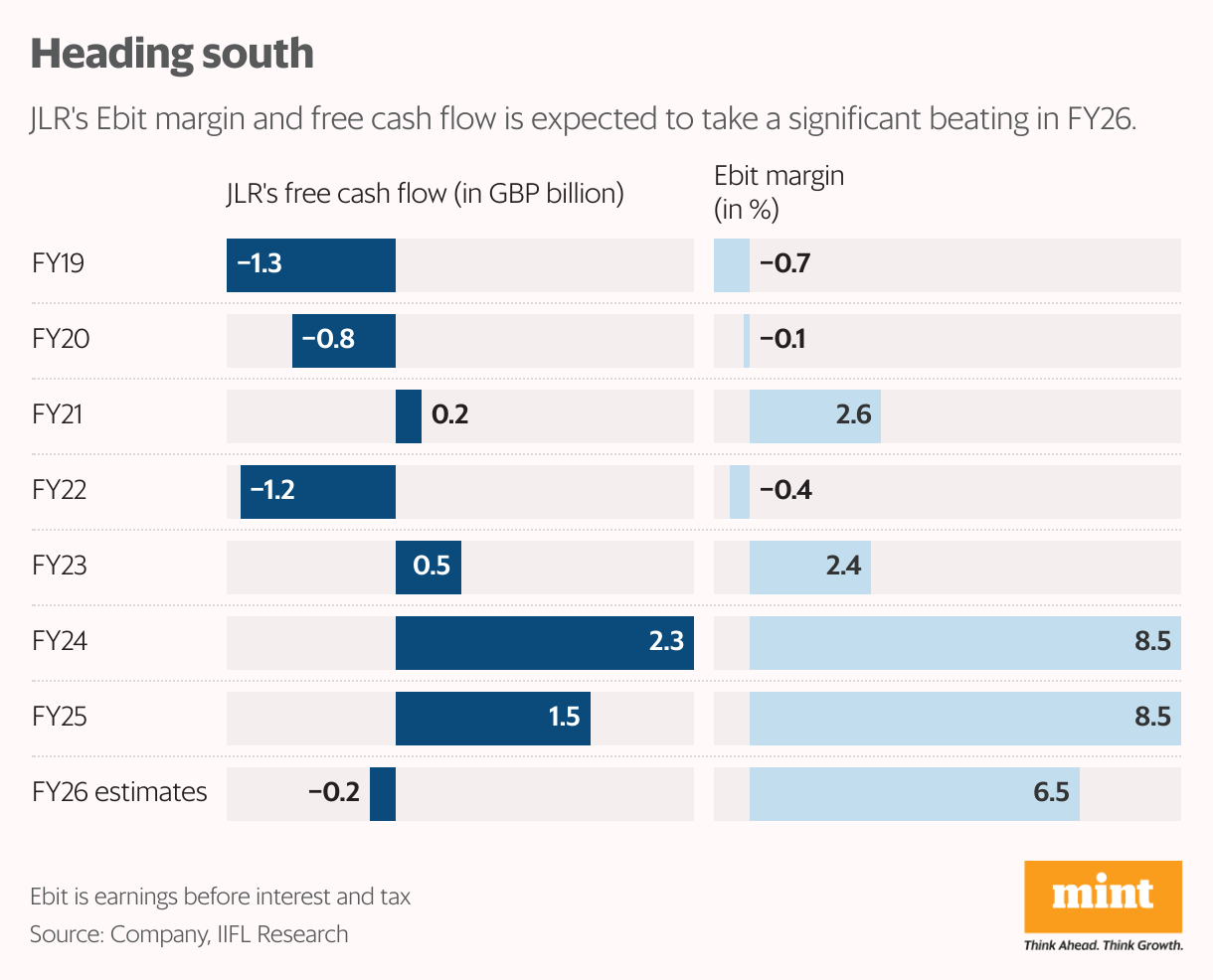

It’s not entirely surprising, then, that at its latest investor day, JLR’s management scaled back expectations on crucial parameters. It now expects an FY26 Ebit (earnings before interest and tax) margin of 5-7%, around 300-500 basis points lower than its earlier guidance. This is also well below the 8.5% margin recorded in both FY24 and FY25, its strongest performance in recent years, according to the company’s presentation.

“The margin guidance at the mid-point assumes that the US-UK trade deal will be effective from the date of announcement (8 May 2025) and that the US-EU deal will be signed before the end of the 90-day tariff pause (14 July 2025),” said a report by BNP Paribas Securities, adding, “Any delay on these deals poses a downside risk to the guidance.”

Read this | Incentives for JLR’s senior executives are now linked to Tata Motors’s market performance

JLR’s FY26 revenue guidance is at £28 billion, as against £29 billion clocked in FY25. A mix of lower margin and higher working capital needs are expected to weigh on free cash flow (FCF). JLR has lowered its FY26 FCF guidance to close to zero from £1.8 billion earlier. This is a significant drop from FCF of £1.5 billion in FY25 and £2.3 billion in FY24.

In view of this, some analysts have cut their earnings estimates.

“While our estimates were already lower than the consensus, we have reduced our FY26 Ebit margin assumption for JLR to 6% (earlier 6.9%), which has led to a 10% cut in our FY26 earnings estimates,” said a Motilal Oswal Financial Services report dated 17 June. The broking firm has maintained its FY27 estimates at this stage.

In response, JLR is taking various initiatives to improve efficiencies across the firm, which should result in cost savings worth £1.4 billion annually over the coming years. With this, it aims to improve Ebit margin to 10% over time.

What augurs well is that JLR has maintained its investment spends guidance of £18 billion over FY24-28, funded from its operating cash flow. Around 50% of this amount is expected to be invested in engineering and the rest in facilities, tooling, etc.

JLR remains central to Tata Motors’ overall performance, as it contributes a significant portion of the company’s business. In FY25, JLR accounted for 71% of Tata Motors’ total consolidated revenue and 80% of profit before exceptional items. Reflecting JLR’s weak outlook, Tata Motors’ shares have declined about 10% so far in 2025, compared with a 5% rise in the benchmark Nifty50.

Read this | Jaguar Land Rover tariff hit compounds Tata Motors’ domestic woes

The company had held another investor meet recently to discuss its domestic businesses where it set targets to improve market share and margin in commercial vehicle (CV) and passenger vehicle (PV). But execution is paramount given the weak demand conditions and rising cost pressures.

As per Kotak Institutional Equities, market share loss in domestic CV and PV businesses remains an area of concern.

Tata Motors believes that the demerger of its CV and PV businesses will help sharpen the focus on each segment. The demerger of the CV business is expected to be completed sometime between September and December 2025.

Also read | Tata Motors plans a premium push as competition intensifies in EV space

Taken together, there is little for investors to get excited about at this stage. In the absence of clear triggers, Motilal Oswal has maintained its ‘Neutral’ rating on the stock, with a sum-of-the-parts-based target price of ₹690 based on FY27 estimates. Tata Motors shares closed at ₹675 on Tuesday.

Leave a Comment