That said, the wealth and asset management segments – with huge growth runways – also continue to perform well and support the overall business. But what’s really driving this shift, and what opportunity could shape the next phase of growth?

We unpack these details in this piece.

Broking under pressure, distribution gains momentum

The wealth management segment includes brokerage, distribution, and lending.

Brokerage has traditionally been a major contributor to this segment’s revenues, accounting for 40% of the total in FY25. As the leading full-service brokerage house, Motilal holds a 7.6% market share in cash and 8.5% in F&O turnover. It also maintains the highest average revenue per user in the industry.

Also read | Maruti Suzuki’s struggle for dominance: Is the EV pivot enough to reclaim market share?

However, brokerage revenue is under pressure owing to a decline in broking volume amid a volatile market and stricter F&O rules. As a result of these, broking revenue fell 37% to ₹166 crore in the March quarter (Q4FY25).

This decline was partially offset by a 140% jump in distribution income to ₹187 crore. While management continues to prioritise the broking business, there is an increasing shift toward distributing financial products.

Why the pivot to distribution makes sense

Motilal sees significant potential in its distribution business, primarily due to the low cross-sell ratio of under 6% among its 40 lakh existing clients. This indicates a substantial growth opportunity, and the low penetration highlights a strong case for expansion.

To tap this, Motilal continues to expand its network of relationship managers (RMs)—a trend seen across the industry—and is targeting a threefold increase in their numbers over the next few years. There is also room for productivity gains as only 33% of Motilal’s current RMs have more than three years of experience. As these numbers increase, so should productivity, driving growth in assets under management (AUM).

This expansion was a key driver of the strong growth in distribution assets in FY25. Distribution AUM accounted for 12% of its segmental AUM at ₹31,551 crore – up 33% from the previous year – as net sales increased fourfold.

For Motilal Oswal, the distribution business could prove to be a key growth driver as it generates recurring, annuity-like revenues. Distribution now accounts for 19% of the segment’s revenue, up from 11% in FY24, while brokerage decreased from 47% to 42%. As this shift continues, stable recurring income from distribution could offset some of the cyclicality of broking.

The opportunity in this space remains large. According to the Knight Frank Wealth Report, the number of ultra-high-net-worth individuals in India is expected to increase by 50% – from 13,263 in 2023 to 19,908 by 2028 – outpacing the global growth rate of 28%. This presents an opportunity worth about $2.5 trillion.

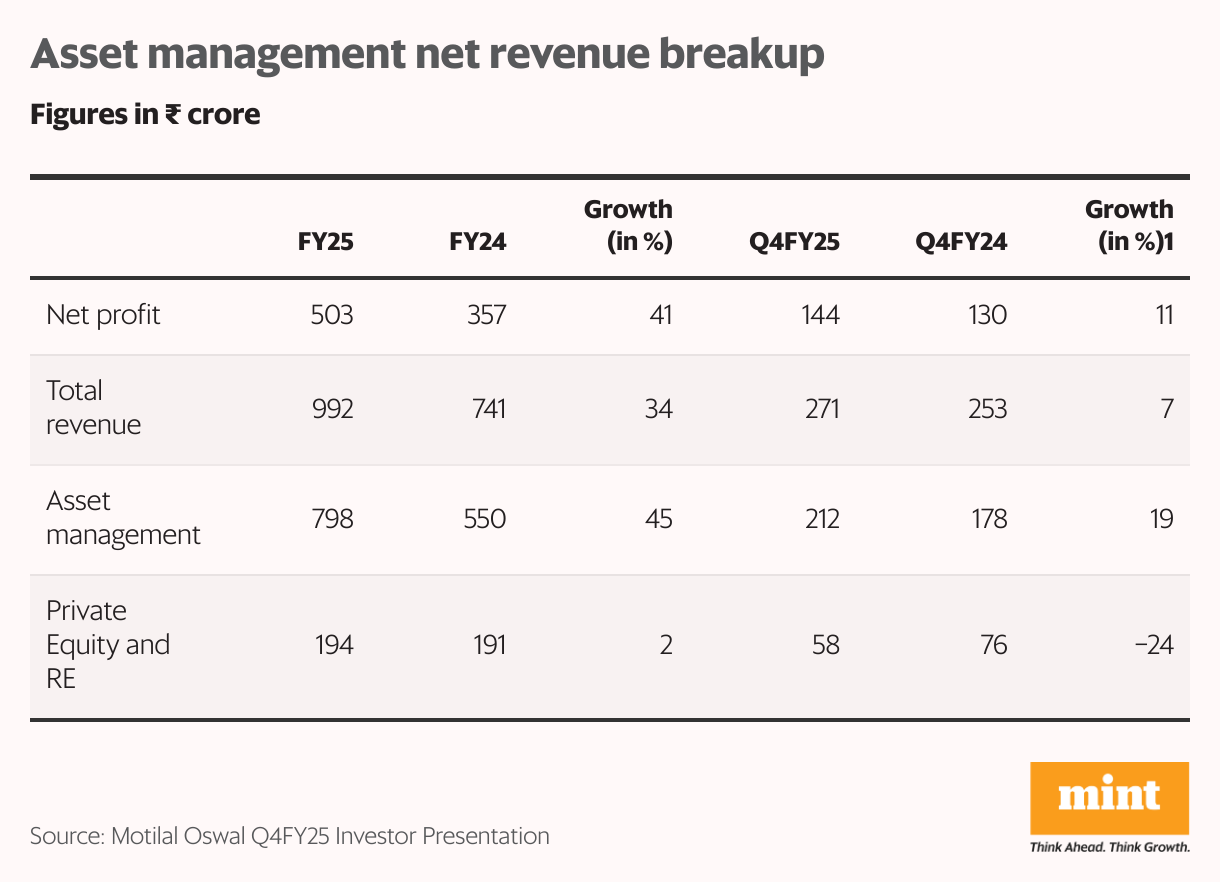

Regaining lost ground in asset management

Motilal’s asset management AUM increased 63% from March 2024 to March 2025, when it stood at ₹1.33 trillion. Mutual funds comprised 93% of this, while the rest came from portfolio management services (PMS) and alternative investment funds (AIFs).

This growth came despite subdued market performance and was driven by strong investor participation. This was reflected in a fourfold increase in gross flows, a threefold rise in SIP flows, and a ninefold increase in net flows over the year.

A key factor behind this momentum was Motilal’s strong hold over individual AUM, which accounted for 88% of the total, well above the industry average of 60%. The company also improved its market positioning by increasing the share of unique folios from 6% in March 2024 to 14% in March 2025.

Fund performance also played a key role, as 90% of its strategies outperformed the benchmark (FY25), placing them in the top quartile. This, coupled with the launch of new funds, boosted gross sales and folio additions. As a result, Motilal regained lost ground, with its SIP market share doubling from 1.5% to 3.2% during the period, and gross sales share rising from 1.6% to 4.3%.

Also read | Force Motors Q4: Strong show, but can the momentum last?

On the financial side, the segment delivered a strong full-year performance. Revenue rose 34% to ₹992 crore while net profit grew 41% to ₹503 crore. However, momentum slowed in Q4FY25, with revenue rising only 7% and net profit increasing just 11%.

Looking ahead, Motilal’s priority is growing equity AUM, primarily through direct channels. It continues to invest in distribution infrastructure, and expand its sales team and branch footprint. These initiatives, backed by positive industry trends and under-penetration of mutual funds, are expected to drive long-term growth despite near-term headwinds.

Private wealth management

Private wealth management serves high-net-worth (more than ₹5 crore) and ultra-high-net-worth (more than ₹25 crore) clients. This segment’s AUM grew 16% in FY25 to ₹1.4 trillion, with net sales doubling during the year.

Segment revenue grew 30% to ₹920 crore in FY25, driven by a 32% increase in recurring revenue and a 29% increase in transaction-based revenue. Net profit grew 28% to ₹321 crore. However, quarterly performance remained weak, with revenue and net profit declining 5% and 6%, respectively, from the same quarter of the previous year.

Private wealth management holds immense potential over the long term, and Motilal, despite being a leader in the industry, lags in the private wealth segment. However, the company believes that regions beyond tier-1 cities hold strong potential. It is looking to expand its presence in these underpenetrated locations – like others in the industry – while expanding its product offerings.

The company expects to continue to grow market share in AUM beyond FY25 levels, driven by strong flows, growth in RMs and client acquisitions. This growth would result in healthy revenue and profit expansion in the private wealth and asset management businesses.

Investment banking posts resilient growth

Motilal’s investment banking business saw strong growth in FY25, completing 39 deals during the year. It topped the qualified institutional placement league table and ranked third in initial public offerings.

Also read: Samhi’s GIC deal may accelerate growth. Could a valuation rerating follow?

With deals worth ₹51,000 crore during FY25, net revenue grew 37% to ₹598 crore, while net profit grew 31% to ₹258 crore. This growth was well supported by a 42% increase in revenue and a 43% rise in profit in Q4FY25.

Going forward, management expects the business to deliver strong growth despite market volatility. To this end, it has appointed a new leadership team, and with its enviable deal pipeline, expects to improve its rank in investment banking.

Fair value losses hit quarterly performance

The March quarter was a setback for Motilal Oswal. The company swung into the red, reporting a net loss of ₹64 crore, compared to a profit of ₹724 crore in the same quarter of the previous year. This marked its first quarterly loss in five years, the last being in Q4FY20.

The loss was primarily driven by a fair-value loss of ₹430 crore, a sharp reversal from the fair-value gain of ₹424 crore in Q4FY24. This also affected its revenue, which fell 45% to ₹1,190 crore in the quarter.

Annual performance stayed strong

However, the poor Q4 was offset by stronger performance in the first nine months of FY25. Revenue increased 17% to ₹8,339 crore in FY25, albeit at a slow rate, while net profit rose just 3% to ₹2,508 crore, weakened by lower revenue.

As a capital markets-led business, Motilal Oswal’s earnings are naturally exposed to cycles. The stock currently trades at ₹666, down about 40% from its 52-week high, and is already pricing in much of the recent weakness.

It trades at a price-to-earnings multiple of 16, which is a discount of about 20% to the 10-year median of 20. A recovery from here hinges on a pickup in market sentiment and stability in earnings.

Nevertheless, the increasing focus on the distribution business and the vast opportunity in asset and wealth management offer tremendous scope for growth. While short-term challenges remain, the long-term outlook remains bright due to the growing financialisation of savings, mutual fund penetration, and increasing number of high-net-worth individuals.

For more such analysis, read Profit Pulse.

About the author: Madhvendra has over seven years of experience in equity markets and has cleared the NISM-Series-XV: Research Analyst Certification Examination. He specialises in writing detailed research articles on listed Indian companies, sectoral trends, and macroeconomic developments. Follow him on LinkedIn.

Disclosure: The writer does not hold the stocks discussed in this article.

The purpose of this article is only to share interesting charts, data points, and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educational purposes only.

Leave a Comment