In times of deep market volatility when stocks are tossed around like sailboats in a storm, the spotlight often turns to the behemoths: large-cap stocks, which are touted to be stable anchors in turbulent waters. Did investors find refuge in these stalwarts during the final quarter of 2024-25, when India’s stock markets continued to slump?

Mint’s shareholding analysis paints a picture of shifting allegiances during the January-March fourth quarter, with foreign portfolio investors (FPIs) shedding holdings, domestic mutual funds standing firm, and individual investors testing the waters.

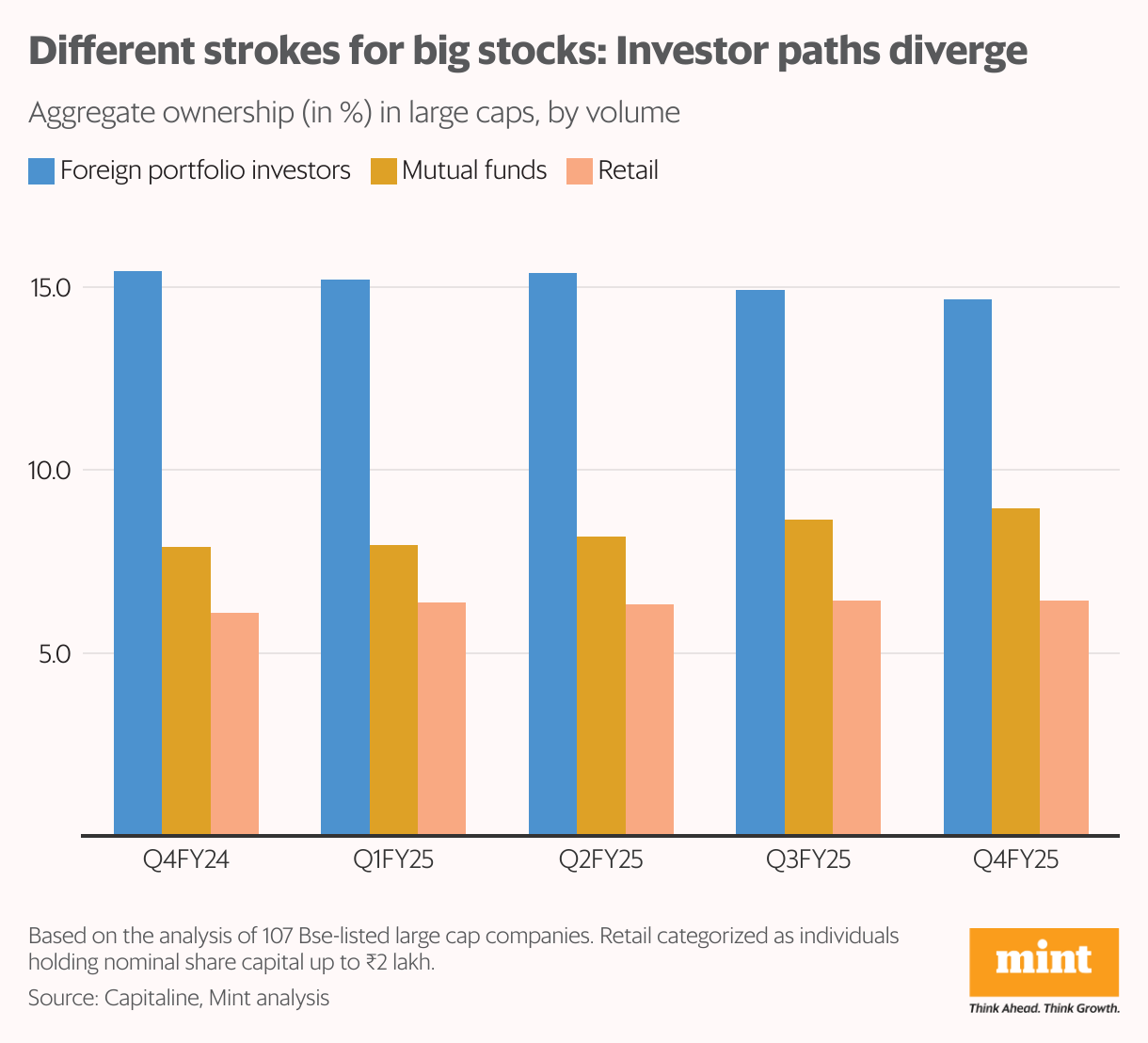

A tale of diverging strategies

In the March quarter, FPIs substantially reduced their exposure to India’s blue-chip companies. Mint’s analysis of 107 BSE LargeCap constituents shows FPIs decreased their holdings in 71% of these firms, marking the most aggressive pullback among all investor categories. This retreat came after a period of sustained selling that began in late 2024 as global investors grew cautious amid rising geopolitical tensions.

Also read | Shareholding moves in Q4: Investors’ verdict on India’s conglomerates

Domestic institutions, however, showed their commitment. Mutual funds sequentially increased their stakes in 70 large-cap firms, or 65.4% of the sample, during the March quarter, continuing a trend of steady accumulation. Retail investors however, adopted a tentative buying approach, increasing their holdings in nearly 40% of these blue-chips while reducing exposure in 57%.

Zooming out

Even viewed from a wider lens, the prevailing sentiment during the fourth quarter was one of cautious maneuvering. On an aggregate basis, in volume terms, FPIs dialed back their exposure in large-cap stocks by 77 basis points over a year to 14.67%. This steady drawdown reflects a growing sense of caution as global growth signals waver and earnings visibility becomes patchy.

Retail investors moderately increased their holdings to 6.4% in the fourth quarter from 6.1% a year earlier, while mutual funds increased their stakes by 1.1 percentage points over the year.

Valuation landscape

What lies ahead? The recent pullback has brought some relief to the stretched valuations. The BSE LargeCap index now trades at price-to-earnings (P/E) of 22.7 times, below its five-year average of 24.7 times. While this suggests improved attractiveness, market experts caution against calling the segment cheap.

Also read | Gold, stocks and FPIs: What the market crystal ball foretells for the next three months

“No, large cap stocks are not cheap, since the markets have run up,” said Utsah Verma, head of research institutional equities at Choice Broking. “While the P/E multiple has corrected from September’s 24.4x to 22.7x, we need to see earnings delivery to justify further upside. The coming quarters’ corporate performance will be crucial,” Verma said in his response to Mint’s market survey.

“We expect market positioning to be bifurcated—domestic-facing sectors like private banks, telecom, consumption, hospitals, and interest-rate proxies will attract more interest due to their relative insulation,” said Neeraj Chadawar, head of fundamental and quant research, Axis Securities. “Export-oriented sectors will stay in wait-and-watch mode. Post the recent correction, select capex-oriented plays look attractive given FY26 growth visibility,” he added.

This is the fourth part of a series of data stories on the latest shareholding patterns. Read the first, second and third articles in the series.

Leave a Comment